www.foolonahill.com

www.foolonahill.com

4. Civil

Aviation Policy in India

6. Passenger

airlines – The players

7. Foreign

equity participation

9. Market

Structure and Implications

10. Trends in International and Domestic Civil

Aviation and Projected Future

Scenario

11. Study of Consumer Demand in the industry

12. Case Study - The No frills model

16. References/Acknowledgements

www.foolonahill.com

1.1

Air

Traffic: The Airport

Authority of India (AAI)

manages total 122 Airports in the

country, which include 11

1.2

Growth:

Estimated

domestic passenger segment growth is at 12% per annum.

Anticipated growth

for International passenger segment is 7% while the growth for

International

Cargo is likely to grow at a healthy rate of 12%.

1.3

Privatization: Privatization of International Airports

is in offing through Joint

Venture route. Three Greenfield airports are getting developed at

Kochi,

Hyderabad and Bangalore with major shareholding of private sector. The

work on

Bangalore airport is likely to commence shortly. Few selected

non-metro

airports are likely to be privatized.100% foreign equity has also been

allowed

in construction and maintenance of airports with selective approval

from

Foreign Investment Promotion Board.

1.4

Air

movements: The total

aircraft movements handled in

October 2003 has shown an

increase of 15.4 percent as compared to the aircraft movement handled

in

October 2002. The international and domestic aircraft movements

increased

by 15.4 percent each during the period under review. The reason

for

increase in aircraft movements is due to increase of operation of

smaller

aircraft by airlines and the introduction of new airlines viz., Air

Deccan in

southern region and international airlines (Air Canada, Polar Air

Cargo, Qatar

Airways (Freighter), Turkish Airways, Air Slovakia at IGI Airport with

effect

from October 2003.

1.5

Passenger

Traffic:

International and Domestic

passenger traffic handled in October

2003 has increased by 15.4 percent and 6.7 percent over the period of

October

2002 leading to an overall increase of 9.4 percent. The total

passenger

increased by 9.2 percent, 7.6 percent, 8.9 percent and 17.0 percent

respectively at five international airports six developing

international

airports, eight custom airports and 26 Domestic airports.

1.6

Cargo

Traffic: The total

cargo traffic handled in

October 2003 has shown an

increase of 3.5 percent as compared to the cargo handled in October

202.

The international and domestic cargo traffic increased by 4.3 percent

and 2.1

percent respectively during the period.

During the month of October 2003, 5346

thousand

aircraft movements (excludes defence & other non-commercial

movements),

40.33 lakh passengers and 88.59 thousand tones of cargo were handled at

all the

airports taken together.

The first commercial flight in

Tata Services

became Tata Airlines and

then Air-India and spread its wings as Air-India International. The

domestic

aviation scene, however, was chaotic. When the American Tenth Air Force

in

For many years in

In recent years, however, this image of Civil Aviation has undergone a

change and aviation is now viewed in a different

light - as an essential link

not only for international travel and trade but also for providing

connectivity

to different parts of the country. Aviation

is, by its very nature, a critical part of the infrastructure of the

country

and has important ramifications for the development of tourism and

trade, the

opening up of inaccessible areas of the country and for providing

stimulus to

business activity and economic growth.

Until less than a decade ago, all aspects

of aviation were firmly controlled by the

Government. In the early fifties, all airlines operating in the country

were

merged into either Indian Airlines or Air

3.1 Need

for Open Skies Policy

A recurring demand often voiced by

interested parties

is that, in order to promote

3.2 Meaning

of ‘Open Skies’

At the outset we must point out that

the

concept of

'Open Skies' is much misunderstood in its meaning and implications.

Strictly

speaking Open Skies means unrestricted access by any carrier into the

sovereign

territory of a country without any written agreement specifying

capacity, ports

of call or schedule of services. In other words an Open Skies policy

would

allow the foreign airline of any country or ownership to land at any

port on

any number of occasions and with unlimited seat capacity. There would

be no

restriction on the type of aircraft used, no demand for certification,

no

regularity of service and no need to specify at which airports they

would land.

Defined in this manner, it is not surprising that Open Skies policies

are

adopted only by a handful of countries, most commonly those that have

no

national carriers of their own and that have only one or two airports.

No sovereign

country of any eminence practices Open Skies least of all the European

Union,

UK, USA, Japan, Australia or countries in South East Asia.

3.3 Bilateral

Treaties

However, almost 99 per cent of

Members of

the

International Civil Aviation

Organization (ICAO) follow the system of negotiated bilateral treaties

determining the aviation

relations between two sovereign Contracting parties. In fact, the

bilateral aviation regime is considered the

fundamental basis for a disciplined and regulated aviation

system between the nations of the world. It provides not

only regularity of operations through scheduled services but also

stipulates

the basis of ownership, number of seats to be utilized, type and

certification

of aircraft and visiting ports of call. The Bilateral Agreements also

protect

the different kinds of aviation

Freedoms granted to contracting parties by specifying the reciprocal

rights to

be enjoyed by each.

3.4 Indian

Bilateral Treaties

3.5 Utilization

of Bilateral Treaty Contracts

It is in the actual utilization of

the

contracted

seats that the problem arises. Of the contracted amount, 50 per cent

are to be

utilized by the national carrier and 50 per cent by the airline owned

by the

contracting country. However, whilst the foreign carriers are in a

position to

use over 70 per cent of their entitlement, the national carrier is only

able to

utilize 29.4 per cent of their share. It is this shortfall that creates

pressure on seats, particularly during peak tourism national carriers

do not

have sufficient aircrafts to be able to utilize the bilateral rights

available

to the country and enter into commercial and code sharing arrangements

to

maximize revenue. Whilst this does improve their profitability in the

short

run, it has a long-term adverse effect in that it deprives the country

of much

needed air bridges to bring in tourists and carry trade.

Under the present bilateral system, the

utilization

of the traffic rights on international routes to and from India, as negotiated by the Government

of India, is restricted to the

two Government owned 'national' carriers - namely Air India

and Indian Airlines and either or both these carriers are

the Indian designated carriers under the various Air services

Agreements. The

Operating Permits restrict the privately owned carriers, such as Jet

Airways

and Air Sahara, to operate only domestic routes within

In the context of a multiplicity of

airlines, airport

operators (including private sector), and the possibility of

oligopolistic

practices, there is a need for an autonomous regulatory authority which

could

work as a watchdog, as well as a facilitator for the sector,

prescribe and

enforce minimum standards for all agencies, settle disputes with regard

to

abuse of monopoly and ensure level playing field for all agencies. The

CAA was

commissioned to maintain a competitive civil aviation environment which

ensures

safety and security in accordance with international standards,

promotes

efficient, cost-effective and orderly growth of air transport and

contributes

to social and economic development of the country.

4.1 Objectives of Civil Aviation

Ministry

a)

To

ensure

aviation safety, security

b)

Effective

regulation of air transport in the country in the liberalized

environment

c)

Safe,

efficient,

reliable and widespread quality air transport services are provided at reasonable prices

d)

Flexibility

to

adapt to changing needs and circumstances

e)

To

provide all

players a level-playing field

f)

Encourage

Private participation

g)

Encourage

Trade,

tourism and overall economic activity and growth

h)

Security

of

civil aviation operations is ensured through appropriate systems,

policies, and

practices

4.2 Private Sector Participation and

the Civil Aviation Policy

·

Private

sector

participation will be a major thrust area in the civil aviation sector

for

promoting investment, improving quality and efficiency and increasing

competition.

·

Competitive

regulatory framework with minimal controls encourages entry and

operation of

private airlines/ airports.

·

Encouragement

of

private sector investment in the construction, upgradation and

operation of new

and existing airports including cargo related infrastructure.

·

Rationalization

of various charges and price of ATF/AVGas will be undertaken to render

operation of smaller aircraft viable so as to encourage major

investment in

feeder and regional air services by the private sector.

·

Training

Institutes for pilots, flight engineers, maintenance personnel,

air-traffic

controller, and security will be encouraged in private sector.

·

Private

sector

investment in non-aeronautical activities like shopping complex, golf

course,

Entertainment Park, aero-sports etc. near airports will be encouraged

to

increase revenue, improve viability of airports and to promote tourism. CAA will ensure that this is not at the cost

of primary aeronautical functions, and is consistent with the security

requirements.

·

Government

will

gradually reduce its equity in PSUs in the sector.

·

Government

will

encourage employee participation through issue of shares and ESOP

4.3

Security

Strict

national civil aviation security programme to safeguard civil aviation

operations against acts of unlawful interference have to be established

through

regulations, practices and procedures, which take account of the

safety,

regularity and efficiency of flights. A good safety record is a judgment of past

performance but does

not guarantee the future, although it is a useful indicator. While

pilot error

is said to be on the decline, factors of fatigue, weather, congestion

and

automated systems have complicated safety. Airline operators, pilots,

mechanics, flight attendants, government regulators and makers all have

a stake

in making aviation as safe as possible. The International Air Transport

Association (IATA), the International Civil Aviation Organization

(ICAO),

manufacturers and others bodies cooperate in this aim. As world air

traffic is

expected to double or more by 2020, the accident rate must be reduced

in order

to avoid major accidents occurring more frequently around the globe.

4.4

Maintenance

Private

sector participation is encouraged in existing maintenance

infrastructure of

Indian Airlines and Air

Air

In

The

AAI operate most aspects of the airport (including air traffic control)

and

procure most of their equipment directly (via global/local tenders).

Until

2000, there were five major international airports, - Mumbai, Kolkata,

According

to projections, Indian air passenger traffic was estimated to grow to

100

million passengers by 2012 from 36.98 million in 1998-99. Growth

projections in

the cargo front were also promising. Airport infrastructure is linked

to

development of

6.1 Indian Airlines

Indian

Airlines was founded in 1953. Today, together with its fully owned

subsidiary

Alliance Air, it is one of the largest regional airline systems in Asia

with a

fleet of 62 aircraft(4 wide bodied Airbus A300s, 41 fly-by-wire Airbus

A320s,

11 Boeing 737s, 2 Dornier D-228 aircraft and 4 ATR-42).

The

airlines network spans from

Indian

Airlines flight operations centre around its four main hubs- the main

metro

cities of

6.2 Air

Air

Air

The

airline is currently undergoing a complete overhaul and restructuring

exercise.

Air

A major investment programme has been launched for the modernization

and

enhancement of its fleet. Fleet review

and route rationalization have become the focus points of Air

Sahara's

strategy. Five new Boeings have been added to the fleet in the last one

year.

These were used to add new destinations and increase frequency on

existing

routes. In the second phase of its expansion four Canadair Regional

Jets have

been added to the fleet this year serve on regional routes.

Air

Air

6.3 Jet Airways

In

May 1974, Naresh Goyal founded Jetair (Private) Limited with the

objective of

providing Sales and Marketing representation to foreign airlines in

In 1991, as part of the ongoing

diversification programme of his

business

activities, Naresh Goyal took advantage of the opening of the Indian

economy

and the enunciation of the Open Skies Policy by the Government of

India, to set

up Jet Airways (

Jet Airways has emerged as

Jet Airways has been voted

6.4 Air

Air

The

company has a modern fleet of ATR-42-320 aircraft, one of the finest

and most

efficient Turbo-Prop aircraft flying. ATR is a European joint venture

between

Alenia Aeronautica and EADS. The ATR 42 has become a reference aircraft

amongst

airlines around the world, by offering a safe, easy to maintain and

comfortable

aircraft operating on the regional market with the best economics on

short haul

sectors. To date, ATR has sold over 650 aircraft to more than 100

operators in

73 countries all around the world.

The

company has adopted a 'lean-and-mean' approach to staffing and aims at

maintaining a low aircraft-to-employee ratio. A good work culture

coupled with

a skilled workforce is the backbone of the company.

While most information

about the Indian Carriers, other than the Government owned, is not in

public

domain, the available information does not tell us much. The Promoters

and Key

Management persons are not listed nor is their equity ownership pattern

provided. Jet Airways' ownership is apparently fully foreign giving

rise to the

phrase:

6.6 Fleet Size

Fleet-wise also Indian

carriers are quite small. Air

This is

minimal when compared with American Airlines, one of the world's

largest

airlines with almost 1000 aircraft and carrying over 80,000,000

passengers and

650,000 Tonnes of freight a year. Even Singapore Airlines, a small

Nation

airline that operates only internationally, has almost twice the number

of

aircraft than its parallel Air

The

three-member enquiry committee, led by former petroleum secretary T S

Vijayaraghavan, has suggested that 100 per cent foreign investment,

including

by foreign airlines, should be allowed in non-scheduled services such

as

chartered aircraft and helicopter operations.

As

of now, foreign airlines are not permitted to pick up equity directly

or

indirectly in domestic air companies. Foreign equity upto 40% and

NRI/OCB

investment upto 100% is permissible in the domestic air transport

services.

Under

the current policy, if a foreign airline operates in

Indian

operators can, however, lease aircraft from foreign companies, but the

government only permits "dry-lease," which requires the aircraft to

be registered in

The US National Commission

to Ensure a Strong and Competitive Airline Industry (1993) envisaged

the

long-term development of more liberal cross border airlines investment.

However, as a short-term measure it advocated ‘expanded access to

international

capital markets by allowing larger investments from foreign investors

under the

current bilateral system’. It also proposed that foreign investors be

able to

hold up to 49 per cent of the voting equity in US airlines, up from the

then

(and still current) limit of 25 per cent.

Any increase in the cost

of equity capital flows through to the choice of debt versus equity and

thereby

distorts capital structures. Airlines should have flexibility in

financing

their operations and developing their corporate structures. The

existence of a cap

on foreign ownership limits this flexibility.

Source -

Business World,

July 2004

Airfares in

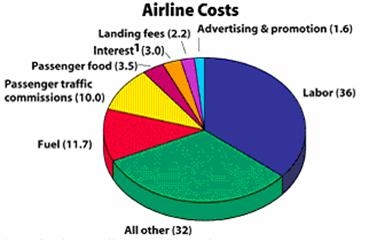

8.1 Labour

If regulations

or industry policy provide protection to an industry, the value of

protection

may be dissipated in poor productivity and higher-than-normal returns

to labour

and capital. Entry limitations

and

capacity constraints have the potential to allow airlines to earn above

normal

returns, which may be appropriated by shareholders or paid out in

higher than

normal costs (including wages, salaries and working conditions).

Given the valuable

contribution that aviation and tourism make to national welfare, it is

essential that the aviation market is globally competitive and

functions in the

most efficient way. This means that the inputs that the industry

depends on,

such as labour and capital, must also be available on an

internationally

competitive basis.

8.2 Fuel Prices

ATF is

the major cost for domestic carriers accounting for 30% of the total

operating

costs in

8.3 Capital

The relatively

capital-intensive nature of the airline industry, combined with the

fact that

airlines are generally regarded as being inherently risky investments,

means

that access to large, well-functioning capital markets is an important

issue

for all airlines. The effects of these restrictions may vary from

country to

country, but are likely to be greater for countries with small domestic

capital

markets.

8.4

Operating Costs

The regulatory system affects where, how

and when airlines can fly. Thus

it affects airlines’ ability to operate efficient networks and their

revenue.

To the extent that airlines cannot use the least cost combinations of

aircraft

types to carry passengers and freight, the costs of operating existing

networks

are higher than they otherwise might be (technical inefficiency).

Further, they

may be prevented from flying the optimum sized and configured network

(allocative inefficiency). Thus, costs may be reduced as airlines are

able to

operate the right aircraft at the right frequencies on an existing

route.

The regulatory system affects where, how

and when airlines can fly. Thus

it affects airlines’ ability to operate efficient networks and their

revenue.

To the extent that airlines cannot use the least cost combinations of

aircraft

types to carry passengers and freight, the costs of operating existing

networks

are higher than they otherwise might be (technical inefficiency).

Further, they

may be prevented from flying the optimum sized and configured network

(allocative inefficiency). Thus, costs may be reduced as airlines are

able to

operate the right aircraft at the right frequencies on an existing

route.

Airlines, by changing the

design of a network and increasing its size, may also be able to

decrease costs

through economies of scale and scope.

8.5 Ownership and control

As

airlines strive for greater efficiencies, they consider the benefits of

consolidation.

However, the normal commercial process of acquisition and/or merger is

not

available due to restrictions contained in bilateral agreements that

are designed

to ensure that ownership and control of airlines remain with nationals

of the

countries where they are based.

Growth

through merger or acquisition enables airlines to achieve economies

scale and

scope by consolidating airline functions. The merger of two airlines,

for

example, may allow them to consolidate their ground handling,

maintenance,

information technology and various managerial functions.

8.6 Airline

Acquisition/Leasing Cost

Taking aircraft on lease is one of the

preferred modes

among the Indian carriers. However, this has suddenly become costlier

affair

due to changes proposed in Union Budget 2004-05. The budget proposes

withdrawal

of tax exemption granted to acquire aircraft or an aircraft engine on

lease

prospectively from

All carriers barring Jet

Airways will feel the heat

of the sudden withdrawal of exemption for taking aircraft for lease as

they

have significant plan to expand the fleet capacity by leasing route.

This

includes both state carriers like Air India (AI), Indian Airlines (IA),

Alliance Air and private carriers like Air Sahara, Air Deccan. As Jet

Airways

that has predominantly prefers owning aircraft rather than going for

leasing.

As tax exemption will not

be available for lease

agreements entered on or after

As leasing route is the

most preferred one for a new

entrant, the Budget initiatives will prove be a heavy deterrent as they

will

escalate the effective lease rental cost by almost 42%.

The aviation industry in

One sees the following characteristics

with respect

to the Indian passenger airlines market –

1.

Few

number of

firms contributing to majority of the market share

2.

Products

are

differentiated in terms of service quality and offerings

3.

MR=MC

4.

p>MC

5.

Entry

Barriers

6.

Firm

is a

price-setter

7.

Long

run profit

>= 0

8.

Strategy

dependent on individual rival firm’s behaviour

9.1 Market

share concentration

According to the figures on market share

of various

scheduled airlines in the same year, Jet Airways topped the list with

46.7 % in

2003-04, followed by Indian Airlines (IA) and its subsidiary Alliance

Air

together at 39.3%, Air Sahara at 13% and Air Deccan 1 %.

9.2 Indian

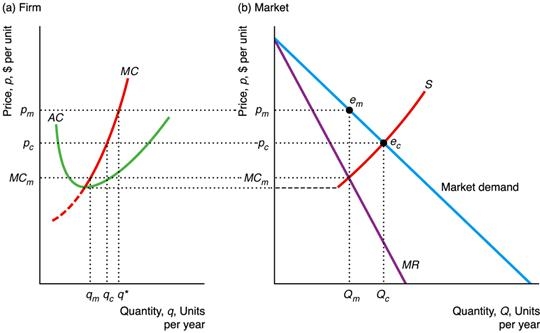

Aviation Market – A differentiated Oligopoly

Each seller in an imperfectly competitive

market

faces a negatively sloped demand curve for his product, permitting him

some

control of the price of his product. In an oligopoly, a few firms

produce the

same product, while in monopolistic competition, many firms produce

differentiated but similar products. In a differentiated oligopoly, a

few firms

produce products different enough for each firm to have its own

downward sloping

demand curve. As with a perfectly competitive firm or a monopoly, the

differentiated

oligopoly firm produces at a profit maximizing level of output where

marginal

cost equals marginal revenue. The firm finds the price it will charge

customers

at the profit maximizing level of output (Qm) from the

demand curve,

and sets price to Pm. As we can see, the firm is earning

economic

profits since price exceeds average total cost at the profit maximizing

level

of output.

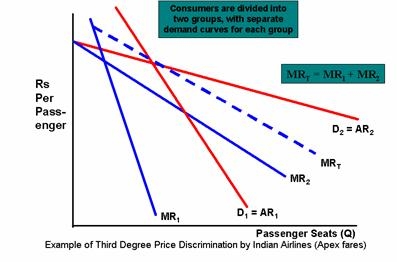

9.3 Pricing

Mechanisms

Price and quantity are determined by the

interaction of demand and

supply in the market. However, given the large number of buyers, firms

can

decide prices at which they will sell tickets. In fact, in the airlines

sector,

firms go in for third degree price discrimination and segment the

market,

charging a higher price to the market with a relatively inelastic

demand (such

as fares between business and economy class travellers, or between

emergency

travel and leisure travel by providing apex fares). The low cost airlines follow this different

pricing strategy. Customers booking early with carriers such as Air

Deccan will

normally find much lower prices if they are prepared to commit

themselves to a

flight by booking early, on the justification that consumer’s demand

for a particular

flight becomes more inelastic the nearer to the time of the service.

Price and quantity are determined by the

interaction of demand and

supply in the market. However, given the large number of buyers, firms

can

decide prices at which they will sell tickets. In fact, in the airlines

sector,

firms go in for third degree price discrimination and segment the

market,

charging a higher price to the market with a relatively inelastic

demand (such

as fares between business and economy class travellers, or between

emergency

travel and leisure travel by providing apex fares). The low cost airlines follow this different

pricing strategy. Customers booking early with carriers such as Air

Deccan will

normally find much lower prices if they are prepared to commit

themselves to a

flight by booking early, on the justification that consumer’s demand

for a particular

flight becomes more inelastic the nearer to the time of the service.

The term ‘‘revenue

management’’ is commonly used to describe most aspects of airlines’

pricing and

seat-inventory c ontrol decisions; but in reality, revenue

managers

primarily practice

seat-inventory control. Formally, revenue management describes a

process of

setting fares for each route (origin and destination pair) and each set

of restrictions

(nonstop, time-of-day, day-of-week, refundable, advance purchase, first

class

or coach, and Saturday-night stayover) and limiting the number of seats

available at each fare. In the language of economics, revenue

management

increases airlines’ profits in three ways –

ontrol decisions; but in reality, revenue

managers

primarily practice

seat-inventory control. Formally, revenue management describes a

process of

setting fares for each route (origin and destination pair) and each set

of restrictions

(nonstop, time-of-day, day-of-week, refundable, advance purchase, first

class

or coach, and Saturday-night stayover) and limiting the number of seats

available at each fare. In the language of economics, revenue

management

increases airlines’ profits in three ways –

·

Implements

peak-load pricing.

·

Implements

third-degree price

discrimination. That is,

fare restrictions screen customers and segment them by their

sensitivity to

price and potentially by their demand uncertainty. For

instance, Indian Airlines apex fares (for

booking one week or three weeks in advance).

·

Implements

an inventory control system for

coping with

uncertain demand.

9.4 Limited

Entry

Virgin Group founder Richard Branson once

famously

said: "The safest way to become a millionaire is to start as a

billionaire

and invest in the airline industry."

The mortality rate in the airline business

is very

high. That's equally true for any low-cost airline model. It requires

adequate

staying power to buy aircraft and take losses in the initial years.

Experts say

it takes nearly $60 million-70 million (Rs 270 crore-315 crore) to

float a

full-service airline.

Entry costs are not

recoverable and incumbents

have the ability to respond quickly to entry of a new competitor.

Capacity

constraints, absence of freedoms to compete on a route, investment

constraints,

and restrictions on codesharing can all be important barriers to entry.

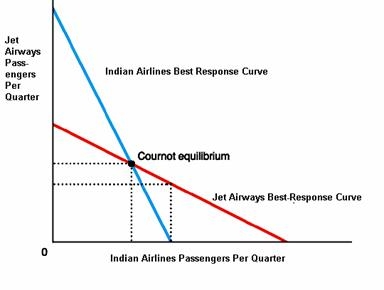

9.5 Market

Equilibrium through the Cournot Model

The revenue of both a competitive firm and

of a

monopolist depends only on the firm's own

output: for a competitive firm we assume that the firm's output does

not affect

the price, and for a monopolist there are no other firms in the market.

For a

duopolist, however, revenue depends on both

its own output and the other

firm's output.

We conclude that the firms' outputs and

the price are

different in Cournot-Nash equilibrium than they are in a competitive

equilibrium. As the demand curve slopes down, price exceeds marginal

cost, so

that, as for a monopoly, the total output produced by the firms is less

than

the competitive output. An implication is that, as for a monopoly, the

Nash

equilibrium outcome in a Cournot duopoly is not Pareto efficient.

Trends

& Alternatives

In 1998, approximately 500

alliances existed between airline companies. Some of these alliances

were to

the point of a merger (Market Share of World Airlines Traffic, 2003).

The scene

today is dominated by a few multilateral alliances. Top three, Star,

Skyteam

and Oneworld together account for over 60% of the total international

traffic.

|

Oneworld |

|

American Airlines,

British Airways, Aer Lingus, |

|

Star |

|

United Airlines,

Lufthansa, Air Canada, Air New Zeland, ANA, Asiana, Austrian, bmi

British, midland, LOT Polish Airlines, Mexicana, SAS, Singapore,

Spanair, Thai Airways, Varig, US Airways, TAM |

|

SkyTeam |

|

Air |

While so far

India has stayed out of these

alliances, relying primarily

on bilateral agreements, it is merely a matter of time before Indian

airlines

are drawn in this web and the three blank spots, Russia, China and

India are

filled in by the International Alliances ((in all three cases, the

leading

carrier is a government owned/aligned entity which makes decision

making a complex

politico-economic process). As it is,

While so far

India has stayed out of these

alliances, relying primarily

on bilateral agreements, it is merely a matter of time before Indian

airlines

are drawn in this web and the three blank spots, Russia, China and

India are

filled in by the International Alliances ((in all three cases, the

leading

carrier is a government owned/aligned entity which makes decision

making a complex

politico-economic process). As it is,

In any case

Considering

the fragmented nature of Indian Aviation Market, at the national level

11.1 The

Potential Market

While formulating the

national strategy one must remember a few aspects of Indian Passenger

Aviation

Market -

a.

Potentially,

b.

Potentially, it is also a very large low-fare

market.

c.

d.

e.

In Aviation circles

11.2

Growing the Market

Airbus Industries Research

shows that there is a cut-off point beyond which the preferred mode of

travel

changes. Thus small distance journeys are convenient by road while

longer

journeys are preferred by rail and air. The data should actually be

viewed in terms

of time involved rather than the distance since technological

development in

any field can impact the time taken for same travel. As has already

happened in

While data for similar

preference change in the mode of travel is not available for

To a business traveller,

overnight journeys by train are quite comfortable although given the

economic

situation even 24 hour journeys are quite acceptable. Beyond that,

given the distances

within the country any one would prefer to hop on a flight provided it

is

offered as an alternate travel service and not something only for the

corporate

world. For this to succeed, the low cost travel will have to be both

with

predictable pricing and longevity of offer beyond the gimmickry of

attention

getting news. This is the only way to enlarge the pie and aim at strata

beneath

the upper crust.

11.3 Other

substitutes

The issue of affordability

of domestic air travel has been well addressed in the Naresh Chandra

Committee

Report on Aviation. While the goal of affordability is absolutely well

placed,

the assumption that the lowering of tariffs, taxes and charges alone;

for fuel,

landing or travel, is the answer that needs careful examination. Even

if these

charges constitute a significant part of the fare, they need to be

evaluated in

the context of competition and monopoly. At home, considering road and

rail as the

competition, the charges for fuel should be viewed as a similar cost

composition for all modes of travel. To reduce fuel charges for any one

sector

while enhancing or retaining them at the same level for the others will

distort

the field. This, particularly when airlines have, and can have, the

freedom of

picking up fuel from other competing nations. Fuel charges at home,

therefore,

should be viewed as a part of the overall petroleum pricing policy.

This is

important since petroleum, as fuel is common to many industry groups

apart from

being a raw material for some. Incidentally, how much of what product

is

extracted from the available crude is as much a matter of choice as is

it a

matter of the quality of crude.

11.4 Low-fare

Airlines

Despite reports of low

budget airlines loosing their momentum due largely to the incumbent

firms’

crushing the competition with even lower fares whenever a low cost

upstart

invaded its market, low-fare will always remain the basic market. This

is amply

proven by the success of Southwest in the

To any buyer of service or

goods, price and quality are always two key considerations. No doubt

there is a

class of air passengers who will only look at the bonuses, be that in

the form of

Frequent Flyer Miles during peak season or extra cushioning of the

seat. These

are generally the corporate travellers where someone else is footing

the bill.

There is also an occasional traveller who, being in distress will not

look at

the price during emergency. While the corporate travellers are a

distinct

segment and will be serviced fully, obviously civil aviation will have

to look

beyond them if it hopes to expand the market. In the US, the low fare

airlines have

almost a 30% share of the entire passenger aviation and in the recent

past

Southwest, the leading Low-fare US airlines has outperformed even the

largest

US airlines in passenger kilometres.

Latest news reports

indicate that the low cost airlines are the price leaders now.

Recently, Southwest

Airlines initiated a round of fare cuts and the bigger airlines had to

respond.

11.5

Consumer

Perception

We

conducted a survey in order to find the consumer perception about

airlines. The

following results have been culled out from the survey of 116

individuals. The

sampling method was a mix of purposive and stratified random sampling

and

attempted to duplicate the general consumer profiles of the population

(as

based on preliminary secondary data). The age group of the sample was

between

18 and 58, across gender, location, and socio-economic class (mapped on

education

and occupation, with a majority of the sample in SEC A and B+).

The region-wise

spilt up of

the sample is as follows:

The areas

covered in the

survey are -

Brand

Awareness Study

Indian

Airlines ranks number one in brand awareness. This could be attributed

to its

long stay in the market and continued support from the government.

Today,

Indian Airlines has become synonymous with reliability and efficiency.

Jet

Airways is offering stiff competition and ranks second in the list.

Usage of Airlines

Indian

Airlines, mostly used by government employees, recorded the highest

usage

followed by Jet Airways. Although most consumers rated Jet Airways high

on

price, it still ranks second in usage and this could be attributed to

its

excellent service and promotion schemes. Similar data for the entire

population

reflects a higher usage of Jet Airways than IA, and a lower usage of

Frequency of Usage

As

indicated in the graph below, a majority the population flies

relatively

infrequently (as compared to the developed markets). Passengers

travelling on

business were found to be more frequent users, while those flying on

holidays

and emergencies were those that tended to make up the segment that flew

less

than once a year.

Note

– As purposive sampling was undertaken at

Flight Class and Occasion of use

Although the occasion of use indicates

that maximum usage is for

business, the flight class graph indicates that the proportion

travelled by

business class is very small in comparison to that travelled by economy

class. This

indicates that most business travellers are flying Economy class as

well. Further,

the second important occasion of usage is for emergencies and

time-critical

travels.

Although the occasion of use indicates

that maximum usage is for

business, the flight class graph indicates that the proportion

travelled by

business class is very small in comparison to that travelled by economy

class. This

indicates that most business travellers are flying Economy class as

well. Further,

the second important occasion of usage is for emergencies and

time-critical

travels.

Circuits Flown: The most frequently flown circuit is that

between

major metros, followed by other state capitals and Delhi-Mumbai.

Scheme Preference: With the entry of new players in the market, airlines are competing for passengers on non-price parameters. This increases the product differentiation in order to decrease elasticity of demand in the market. Given the key differentiators that substitute for price, consumers have rated Apex fares as their most preferred scheme. Indian Airlines, Jet and Air Sahara offer apex fares. Next most preferred to Apex fares is the frequent flyer program, a trend noticed predictably in the high frequency repeat users and those travelling on business.

Factors

affecting consumer perception

We

identified the following factors that make the demand function of

consumers.

Based on our hypothesis, a choice parameter weight was arrived at by

asking the

sample to rank the following parameters on a Likert scale -

a)

Price

b)

Service

c)

Promotional

Schemes

d)

Loyalty

programmes

e)

Flight

Schedules

f)

Comfort

with the

brand

g)

Corporate

tie-ups

Price appears to be

most important factor

for the

consumer followed by service provided and flight schedules.

Price appears to be

most important factor

for the

consumer followed by service provided and flight schedules. Indian

Airlines has been rated high on most parameters while Jet Airways,

although

rated low on price, is rated highest in most other factors. Air

Air

Sahara’s many services such as In-flight entertainment and Wings n'

Wheels

coach service, exclusive business lounges being operated at departure

halls at

airports in a number of cities, providing for business and refreshment

services

has made it second most popular under services. It has taken the lead

in

introducing novel initiatives such as Steal-a-seat flexi fare options,

Sixer/Super

Sixer and Square Drive/Super Four.

Air

Sahara's frequent flyer program called Cosmos has also become a great

hit with

the passengers, though it still ranks almost on par or lower on

customer

perception than the schemes offered by Jet and IA (see promo schemes

and

loyalty programs), essentially due to lower customer awareness levels.

Corporate

tie-ups were a trend significant by their absence on the brand

preference

parameters. While the only major tie-ups were by Indian Airlines with

government agencies, these were not perceived as strictly ‘corporate’

tie-ups.

This segment is hence a possible opportunity which can be explored as a

non-price differentiator, given the large frequency of use by business

travellers.

12.1 Analyzing Southwest

Airlines

and how, in

Southwest

Airlines Co., incorporated in 1967, is a

As

of

Presently,

Southwest is the third largest

So

what differentiates Southwest from the ‘legacies’?

·

Southwest's

average aircraft trip stage length in 2003 was 558 miles, with an

average

duration of approximately 1.5 hours.

·

The

Company's point-to-point route system, as compared to hub-and-spoke,

provides

for more direct non-stop routings for customers and, therefore,

minimizes

connections, delays and total trip time.

·

Southwest

focuses on non-stop (not-connecting) traffic. As a result,

approximately 79% of

the Company's customers fly non-stop

·

In

addition, Southwest serves many conveniently located satellite or

downtown

airports such as Dallas Love Field, Houston Hobby, Chicago Midway,

Baltimore-Washington International, Burbank, Manchester, Oakland, San

Jose,

Providence, Ft. Lauderdale/Hollywood and Long Island Islip airports,

which are

typically less congested than other airlines' hub airports. This

enhances the

Company's ability to -

1.

sustain high employee productivity

2.

ensure reliable on time performance

3.

lower landing and parking fees

4.

achieve high asset utilization

·

Aircraft

are scheduled to minimize the amount of time the aircraft are at the

gate

(approximately 25 minutes), thereby reducing the number of aircraft and

gate

facilities that would otherwise be required.

·

The

Company operates only one aircraft type, the Boeing 737, which

simplifies

scheduling, maintenance, flight operations and training activities.

·

Southwest

does not interline or offer joint fares with other airlines, nor does

it have

any commuter feeder relationships.

·

Southwest

offers a ticketless travel option,

eliminating the need to print and process a paper ticket altogether. In

2003,

more than 85% of Southwest's customers chose the ticketless travel

option and

approximately 54% of passenger revenues came through the Internet.

For

the past five years, low-cost airlines have been growing at more than

40 per

cent a year, while the full-service airlines are yet to recover from

the crisis

that hit them post 9/11. Taking a cue, Capt. G R Gopinath launched Air

Deccan in September 2003,

·

Airbus

320 can

accommodate 180 seats while IA has 145 seats including executive class.

The

extra 35 seats are in Rs 500-Rs 2,500 bracket

·

In

contrast to

the hub-and-spoke model, Air Deccan follows the point-to-point concept,

which

removes hindrances like waiting for connecting flights and through

baggage

check-in

·

Result:

greater

flexibility. Each Airbus 320 flies for 10-11 hours compared to the 7-8

hours

clocked by other airlines

·

Air

·

The

model is

akin to any other low-cost carrier. Even the most expensive ticket on

offer is

35 per cent lower than usual fares on any sector. In the

Delhi-Bangalore sector

for instance, the first 40 seats are available between Rs 500 - Rs

2,500, the

next 110 seats up to Rs 5,000 and the remaining don’t cross Rs 7,000.

·

Unlike

IA, Jet

and

But

unlike low cost airlines in the

·

Air

·

Plans

to launch

services on trunk routes have been delayed as it has not been allotted

parking

bays and ticket counters in Mumbai and

·

The

operations

of Air Deccan to Guwahati and Dibrugarh are not by choice but are part

of the

Category 2 and Category 2A routes which are compulsory for a private

airline

operating on metro routes. This need for compliance though has bled

full-service airlines what with their larger capacity fleets.

Others

are just as keen to get

All

this activity has spurred

The

new players face some serious hurdles. The biggest is infrastructure.

Indian

airports are dismal -- when cities are lucky enough to have one. Even

cities

with millions of inhabitants -- such as

High fuel costs and other

operating fees such as landing and parking charges, which account for

up to 15

percent on an airline's expenditure, have kept air fares high and

grounded most

carriers which have entered the domestic aviation sector when it opened

up

nearly a decade ago.

Defining

Low Cost Carriers

Simple Product

Positioning

Low Operating Costs

Attributes

of Low-cost Carriers

·

Narrower

seating

(higher capacity: 148 vs. 126)

·

Higher

plane

utilization (10.7h vs. 8.4h) due to shorter turnaround times

·

Lower

staff

costs due to greater productivity, generally lower wages and smaller

staff (no

service)

·

Lower

airport

fees at secondary airports and smaller cities

·

No

sales commissions

due to web sales

·

Low

station

costs due to simpler handling and more efficient processes

·

High

number of

passengers per employee - 7250 for RyanAir vs 1290 for Lufthansa (2002

data)

Strengths

·

Passengers

will

continue to need connecting/network services

·

Ensure

a leisure

travel, especially to the business traveller, like airport lounges

·

Enhanced

in-flight service and more comfortable seating

·

In

long-haul

markets, where premium service is essential, through higher capacity

and long

range Boeing 747s and Airbus 340s.

Weakness

·

Excess

capacity

·

Complicated

flight operations. Hub-and-spoke networks of legacy carriers were

profitable as

long as LCCs had low service along heavily travelled routes.

·

Mounting

debt –

Enormous debt to investment ratio (above

90% for most

·

Cost-to-revenues

ratio per seat mile is very high (>13) compared to Southwest’s 7.67

Opportunities

·

Maintain

short-haul flights only to extent needed to feed the network

Threats

·

Labour

problems as “legacies” try to streamline in order to compete with

LCCs

·

Flood

of new

capacity into the region from LCCs may trigger a competitive bloodbath

among

the legacies.

No-Frill

Airlines Prices

This

cut throat competition is at its peak in sector like Delhi-Mumbai where

Jet

Airways has cut its Apex air fare to Rs 2500 for passengers booking

ticket 30

days in advance. This was in response to Indian Airlines concessional

fare of

Rs 3500 if ticket is booked 21 days in advance and Air Sahara’s special

package

offer of Rs 4444 for a return ticket basis. The no-frills airline Air

Deccan

has announced fares as low as Rs 700 if booking is done 90 days ahead.

Jet

airways has lowered its apex fares by 20% under ‘Monsoon Super Apex

Fares’

scheme if the booking is done 30 days in advance in six busy sector

including 4

metros.

15.1 Government

Recommendations

Codesharing

Codesharing is an

important tool for airlines to minimise the costs of operating

services. By

selling seats on a flight operated by another carrier, codesharing

enables an

airline to make direct cost savings by rationalising services or

establishing

market presence on a route without actually operating on it. Thus, both

airlines

may be able to save on fuel, labour and other variable costs, as well

as making

more effective use of aircraft and other overheads.

Cabotage

Restricting access by foreign

carriers to the Indian domestic market gives the Indian carriers a

solid base

from which to extend into international aviation. The same applies to

most

other countries, with the exception of city economies such as

·

operational

synergies and efficiencies by

being able

to switch capacity and aircraft between the domestic and international

sectors;

and

·

network

advantages such as economies of

scope and

traffic density as well as the marketing advantages of operating a

combined

domestic and international network.

The opposition to this

recommendation is the view that It is most

likely that foreign

carriers would engage in ‘cherry picking’ i.e. carry domestic traffic

on the

most profitable routes. Incumbent airlines would need to counter any

loss of

profitability on routes affected by cabotage and this could mean a

reduction in

the number of services provided on these routes, or the reduction or

withdrawal

of services from less profitable routes, with consequential loss of

amenity to

passengers, including those making connections to other parts of the

domestic

network.

The regulatory

structure inhibits competition in many ways. It can prevent or deter

entry,

constrain capacity, and limit the potential for airlines to win market

share. A

problem in assessing regulatory impacts is the structure of aviation

markets. Economies

of scope and traffic density favour large airlines operating many

services. On

the demand side, a single carrier operating a long thin route with

multiple

frequencies will attract better business than multiple carriers who

each operate

one service per week. Thus markets tend to be concentrated with a small

numbers

of carriers operating on most routes.

It cannot be presumed that these airlines

respond to normal commercial incentives.

Instead of shareholder value, they may be managed for national

prestige,

employment enhancement, technology transfer, or defence, which might

require

government subsidies. Continued use of substantial government subsidies

is an

obstacle to efficient air services, and has important implications for

competition in a less regulated international environment.

Eliminate

the fuel tax

A most regressive

tax whose burden becomes larger as fuel costs increase (and airlines’

ability

to pay diminishes). As an interim step – cap tax revenue and determine

a better

way of obtaining (e.g., a per passenger levy).

Eliminate category III

restrictions

Eliminate

category III restrictions and provide essential air services subsidies

where

required (with costs shared by national/state/local authorities).

Category III

mandates that an

operator

deploy on routes in Category-II (North-Eastern

region, Jammu & Kashmir, Andaman & Nicobar and Lakshadweep)

at

least 10% of the capacity deployed on routes in Category-I and of the

capacity

thus required to be deployed on Category-II routes, at least 10% would

be

deployed on service or segments operated exclusively within the

North-Eastern

region, Jammu & Kashmir, Andaman & Nicobar and Lakshadweep. In the interim, allow airlines to

transfer category III obligations to a competitor or third party

operator – who

could use a standard, appropriate fleet and be paid by the majors to

meet their

category III requirements.

Improve quality of and

access to airports and hangars

Privatize or municipalize.

Develop a robust traffic management system that addresses relevant

technical

issues and meets strategic objectives through rigorous systems

engineering and

large-scale integration efforts such that rising air traffic demand is

supported in a safe, secure and efficient manner.

Today, Indian

airlines have difficulty accessing hangars for maintenance. As a

result,

private operators have to do some maintenance abroad. Airline

maintenance and

overhaul should be an area where

Tourism

An efficient

aviation sector is essential to support the tourism industry, which has

immense

employment opportunities and the tourism and airline industries with a

joint

proactive approach can foster tourism development and promotion in a

big way.

One of the prerequisites for developing tourism is 'easy access' to the

tourist

destinations, in terms of international and domestic connectivity and

easy

movement within the destination. An efficient aviation sector is

essential to

support tourism. Air connectivity is integral to the growth of tourism.

Airlines and tourism are self dependent. The tourism market grows by

itself

with new connections and a popular destination attracts more flight

operations.

It is a win-win situation.

Direct

connections would also give further impetus to tourists’ arrival. Over

40 per

cent of the passenger traffic is concentrated in two main international

airports namely

15.2 Industry Recommendations

Reduce labour

costs

All

major carriers need to win significant concessions from their workers.

Low

labour outlays would consist of a mix of reduced wages, more flexible

work

rules and trimmed benefits including pension.

Simplify

flight operations

Low-cost carriers use just a

few types of aircraft, a strategy

that cuts training and maintenance expenses. Larger airlines who fly

internationally, to more remote destinations require varied fleets of

large and

small planes. However, they can and should work toward streamlining the

types

of planes they fly.

Another way to simplify operations is modifying the hub-and-spoke

model, which

uses designated headquarter airports for transfers. Traditionally, the

big

airlines have sent many of their flights through hub airports at peak

business-travel hours. That way, since carriers typically charge heaps

more for

business fares, they can get more revenues per flight. But many experts

argue

that it's time to give up on that model - especially as low-cost

carriers

increase service along heavily travelled routes.

Experts like the idea of so-called rolling hub operations, where

flights are

scheduled throughout the day so that an airline's assets - from

employees to

planes to hangars - can be used more efficiently. In a traditional hub

system,

planes and workers spend more time waiting for connecting flights to

come in at

peak operating times. With rolling hubs, travellers may end up waiting

a little

longer to get a connecting flight, but planes end up in the air for

more hours

of the day.

Offer more

transparent pricing

The legacy

carriers have long had an exotic,

almost incomprehensible pricing system. However, these days, with the

Internet

allowing travellers to shop for the cheapest tickets easily, and

low-cost

airlines offering uncomplicated set prices, traditional carriers have

to follow

suit or risk losing more and more passengers.

Get smart on

fuel

With

oil near $50 a barrel, airlines must be smarter about how they

incorporate its

price into their costs. Discount carriers such as Southwest hedge as

much as

80% of their jet-fuel costs. Essentially, that means that they lock in

prices

on future fuel when the price drops. Small wonder Southwest is one of

the few

success stories in the airline business.

Stop chasing

market share

Airlines

need to be savvier about capacity. At the start of 2004, many planned

to add

more flights amid signs of an improved economy. When it became clear

that

demand wasn't as strong as originally forecast, most carriers still

wouldn't

retrench from their plans for fear of losing out if the market snapped

back.

Rather than scrambling to add seats in fear of missing out on the

party,

airlines would do well to take a more cautious approach and focus on

efficiency

and margins.

From bailouts

to government partnership

Although

the Indian airline industry was largely deregulated in 1990, plenty of

lingering rules and regulations have made it nearly impossible for

carriers to

be efficient. Many believe that restrictions on foreign ownership and

labour

laws have kept the industry from innovating. So instead of lobbying for

protective measures like bailouts, airlines need to work with

government to

tackle longer-term projects like building more runways, running

airports more

efficiently, and reining in labour costs.

A new model

for premium pricing

Most

of the industry's improvement efforts have focused on whittling down

costs.

However, boosting revenues also needs to be a priority. After all,

people are

willing to pay more if they believe they're getting more value. Legacy

carriers

still offer certain advantages, especially to the business traveller

including

airport lounges and more comfortable seating.

·

White

Paper on ‘

·

The

Civil

Aviation Act, 2000 (Draft)

·

Aviation Week & Space

Technology

·

Low-fare

Airlines, (2004, July 8).

Economist.com.

·

Crisis

at 50, Business World,

·

Businessline,

·

The

Sky’s The Limit, Indian

Express

·

Oil

Prices drown out Airlines profit, Star Tribune,

·

A Feel for Airline Security. Time

·

To

Cope With Travel Slump, Airlines Turn

to Smaller

Jets. (cover story) Wall

Street

Journal - Eastern Edition, Sept. 2004

·

Wikipedia,

the

free content encyclopedia

·

·

Discounted

IA fares to take on no-frills